Are low-cost mutual funds or ETFs better investments in a tax-advantaged account? Also, more strategizing from that SECURE Act 2.0 529 plan provision, the pros and cons of selling a rental house now or holding it until you pass, and an easy-breezy self-employed retirement account that’s better than a SEP IRA. Plus, will municipal bond income bump you into a higher tax bracket? Can you avoid capital gains tax by investing less aggressively over time?

Show Notes

- (00:46) Mutual Funds vs. ETFs in a Tax-Advantaged Account? (Midwestfabs, St Paul, MN)

- (08:06) SECURE Act 2.0 529 Plan Strategy (Chris, Atlanta)

- (14:51) Will Municipal Bond Income Bump Me Into a Higher Tax Bracket? (Bobby, Philadelphia)

- (26:31) Can I Avoid Capital Gains By Investing Less Aggressively Over Time? (Joe, Aston, PA)

- (33:12) Pros and Cons of Selling a Rental House Right Now (Joe, Chula Vista)

- (34:48) An Easy Breezy Self-Employed Retirement Account Better than the SEP IRA? (Steve, Las Vegas)

- (39:58) The Derails

Free financial resources:

LISTEN | YMYW Podcast #325: Capital Gains Tax Vs. Ordinary Income Tax Explained

READ THE BLOG | Small Business Tax Filing: A Helpful Guide – with Self-Employed Tax Strategies, 5 Impacts of the Tax Cuts & Jobs Act on Small Business Owners, and the Qualified Business Income Deduction

Listen to today’s podcast episode on YouTube:

Transcription

Are low-cost mutual funds or ETFs better investments in a tax-advantaged account? That’s today on Your Money, Your Wealth® podcast 420. Also, more strategizing from that SECURE Act 2.0 529 plan provision, the pros and cons of selling a rental house now or holding it until you pass, and an easy-breezy self-employed retirement account that’s better than a SEP IRA. Plus, will municipal bond income bump you into a higher tax bracket, and can you avoid capital gains tax by investing less aggressively over time? And, we’ve got three Joes on today’s show I’m producer Andi Last, and here are the host of Your Money, Your Wealth®, our first Joe, of course, is Joe Anderson, CFP® along with Big Al Clopine, CPA.

Mutual Funds vs. ETFs in a Tax-Advantaged Account? (Midwestfabs, St Paul, MN)

Joe: Uhh…

Andi: Midwestfabs.

Joe: Midwestfabs from St. Paul, Minnesota. “Hello again from the banks of the mighty Mississippi River. Thanks for taking the time and shedding some light on my employer match question and directing me to the video links, white papers, et cetera, dedicated to the nuances of the SECURE Act 2.0. Good stuff.” I have no idea what the hell he’s talking about.

Andi: He asked you to do several shows about the SECURE Act.

Joe: Oh, did you send him a bunch of stuff?

Andi: I sent him stuff. We talked about stuff that was available, so, yeah.

Joe: So you and Midwest Fabs are like tight buds.

Andi: All of us are, we’re all buddies.

Joe: Got it. “After listening-“

Andi: “-between the ears-“

Joe: “- between the ears, dedicating a few shows to the nearly 350 or so pages of the SECURE Act embedded within the 4000 or so pages of the spending bill was not on top of YMYW’s to-do list. My questions are about asset vehicle location.”

Andi: So in other words, he accepts the fact that you were rejecting his request for several shows on the SECURE Act.

Joe: Yeah. Cause there’s not much there.

Al: I mean the bullet points you can get from Googling it and you’ll know almost what you need to know.

Joe: There’s thousands of pages of just nonsense.

Al: And a lot of it’s the spending bill, which has nothing to do with what we’re talking about.

Joe: Right. I mean, the big things on the SECURE Act is probably, you know, 3 or 4 things that we’ve already mentioned multiple times. You know, the RMD has changed, the 529 plans. Then there’s some, a lot of different changes to overall retirement plans, the Rothification of things, increased matches, you know, but it’s not going to really secure every neighborhood’s financial future or whatever the hell’s secured-

Al: As it was illustrated.

Joe: Yep.

Al: Yep. It helps, a little.

Joe: It does. “If one has a choice-“

Andi: -between-

Joe: I, I, I got, that kind of took me off there. BW, I wasn’t sure what BW means. Between-

Al: B slash W-

Andi: To me that’s black and white.

Joe: Is it black and white or between?

Andi: It’s between.

Al: I had no idea what that meant, but anyway, you’re right. That’s it. Makes sense- between.

Joe: “If one has a choice between a low cost index fund or a similarly structured ETF, does it make a difference in a tax advantage account in which one someone should use? How about taxable type of account? Aside from expense ratios, what else should one consider when deciding which investment vehicle to use and where?” Okay, there’s more to this. “I would think that in tax advantage accounts, regardless on how the underlying fund is traded, capital gains, losses, dividends, et cetera, it should not matter. But choosing a mutual fund or ETF in a taxable account might not be as advantageous due to the unwanted creation of potential taxable events associated with a mutual fund. Currently a-“

Al: -varietal?

Joe: -varietal? “- varietal Growler 6-pack- Growler. Oh, there you go. Growler. I know what that is. “-6-pack from the Steel Toe Brewing Company in St. Louis Park-“. Steel Toe Brewing. Okay. Steel Toe Brewing.

Al: You know them?

Andi: They’ve got an IPA, they’ve got an ale.

Al: That’s kind of your old, stomping grounds. Probably new since you left though.

Joe: Yeah. I grew up really close to St. Louis Park. I played them in high school. I went to Robinsdale Cooper High School. Oh yeah. St. Louis Park was our rival.

Al: Nice.

Joe: Yep. “-in a rotation in the basement fridge.” See? Basement fridge. You can tell he’s from St. Louis Park. So but, you know, higher class. A little bit richer neighborhood than when I grew up. We had a garage fridge. So he, he likes a little Steel Toe, Brewery there. All right. He’s got the basement fridge. “I also have a new walking companion, named by the rescue organization, Jake from State Farm, to accompany me while I digilently – didg – DILIGENTLY keep up with the best podcast on the interweb.”

Andi: This is Jake from State Farm on screen right now.

Andi: This is Jake from State Farm on screen right now.

Al: Oh yeah. Very cute. Looks, looks friendly.

Joe: “Many thanks for the simplicity, real and funny spitball wisdom you share with the YMYW tribe.” Why the hell do I feel like I’m drunk now?

Andi: It’s been all that Steel Toe IPA.

Al: You’re thinking about beers.

Joe: I know. Now I’m all foggy brain. “Congratulations to Andi for her newly bestowed title by another YMYW listener of the Boss Lady. Cheers. Midwest Fabs.”

Al: Yeah, she kind of controls us, doesn’t she, Joe?

Joe: She is the Boss Lady.

Andi: I try to keep this 3-ring circus within the 3 rings.

Al: And you do a great job. Or so we’re told. Joe and I actually don’t listen to the podcast, cause we’ve already done it.

Joe: I could barely stand making it through it, let alone spend another hour listening to it. So I don’t even know what I’m –

what’s his question?

Al: Here’s the question. ETFs versus low-cost mutual funds, which is better in a non-retirement account, non-qualified account? And I would say ETFs are slightly better. To be perfectly honest, both are super tax efficient, but the most tax efficient would be an ETF. Because, in a index fund, sometimes the fund manager has to liquidate funds, you know, sell stocks for distributions requested by investors, and then that means everyone gets their pro rata share of that capital gain. So you get those capital gain dividends right at year end. In a ETF you’ve got far less of that because generally when someone needs to liquidate, they’ve liquidated their own unit and it doesn’t affect you. Otherwise, and that that’s not like a huge difference. But it is slightly better, I would say to have an ETF.

Joe: Yeah, the structure of an ETF is a little bit more tax efficient, but if you’re in an index fund, just realize there’s not a ton of turnover in index funds.

Al: Yeah, that’s what I’m saying. It’s not that much different. Now if you’re invested in an actively traded mutual fund, that’s completely different. Because now you got a fund manager trying to beat the market and they’re buying and selling all the time, which causes a lot of capital gains, which you’ll have to pay for.

Joe: Or unless you are in this fund company that is very large, Vanguard. I think they changed like what, to admiral shares or they did something. And then they, every, I mean, people got hit pretty hard with the capital gain, even though they’re indexed fund and they’re very tax efficient. But-

Al: So yeah, if you have a choice, all things being equal, I would go ETF. But yeah, certainly the fund expenses are very important. I’d rather go for a cheaper index fund than a more expensive ETF.

SECURE Act 2.0 529 Plan Strategy (Chris, Atlanta)

Joe: Got Chris from Hotlanta. “Andi, Joe, Big Al, longtime listener, first time caller with a question about a Roth IRA wrinkle in the SECURE Act 2.0. First the facts, 49-year-old, high earner, married to a 43 year old, even higher earner, and we just had a beautiful baby girl in September of 2022. We got a little crazy at the end of Covid and couldn’t be happier first time parents. Does this sound familiar, Joe?” Hey, now.

Al: That’s getting pretty close to home, huh?

Joe: Ouch. Oh my God. We’re blood brothers. Yeah. Little COVID babies.

Al: I feel like I know Chris.

Joe: Yeah. He does a little podcast down in Atlanta. Yeah. Very similar kind of situation here. He’s a little bit older than me.

Al: Oh yeah. What, a year?

Andi: Negative 6 months?

Joe: Yeah, Chris is an old man. See, I’m young and spry.

Andi: Especially with those two kids in the house.

Joe: Yes. Oh man. Yeah. Year and a half- time goes by-

Al: Yeah, it does go by fast, doesn’t it?

Joe: “I drive a 2014 Toyota 4Runner Limited, and my wife’s has a 2013 Audi A4 Quatro. Our drinks of choice is a cold Miller Life for me, a vodka soda or gin and tonic for the missus, or a nice glass of California Cabernet if we are feeling fancy. We have about $1,200,000 in a rollover traditional IRA, $300,000 in Roth IRAs, $250,000 in a Roth 401(k), $25,000 in our HSAs, and $200,000 in a brokerage account or cash and $500,000 in investment real estate equity. I’m always looking for more ways to get our dollars into Roth accounts. Reading up about the SECURE Act 2.0, there is a provision that addresses flexibility on 529 plans that I believe might be another opportunity. From the article, a concern among parents saving in a 529 plan is the chance their child chooses to skip college, or the funds may go unused. In this scenario, parents can pass the account to another beneficiary or withdraw funds for non-qualified expenses resulting in income tax and a 10% penalty on the earnings. When 2024 rolls around, parents will have another option. A SECURE 2.0 provision allows the tax and penalty-free withdrawal rollovers to Roth IRAs from 529 college accounts that have been open for at least 15 years. There’s also a $35,000 lifetime limit on these transfers per account beneficiary, plus a few other limitations. I’ve already opened and seeded- seed funded a 529 plan for my daughter. My question is if I can open two additional 529 plans, one for my wife and one for me, and fund them each with after-tax dollars.

They will then grow tax-free for the next 15 years. After that point, could I then either transfer them to my daughter if need be? Or could we just convert them to Roth IRAs for my wife and be keeping in mind the $35,000 limit mentioned above when/if we don’t need them in our lifetime? My daughter would then inherit them at some point down the line. Is this a viable strategy? And if not, what am I missing? Chris.” Sounds like a lot of work for really not a lot of benefit.

Al: Well, yeah, because of all those limitations and, and so the $35,000, you can’t do all in one year. You’re limited to the amount that a Roth contribution or traditional IRA contribution would be, which right now is $6500. So anyway, you could do that, you know, when you’re over 50 you can do $1000 more, so $7500. So you can do that every year. You have to have earned income. So both of you would have to have earned income. And when you’re in, say your 60s or close to 60s, in case of your wife, so gotta have earned income to do this. And it would count against any other Roth contributions that you would otherwise make. You can’t do both, right? Oh, you do one or the other, or a combination. So I tend to agree with you, Joe. It does seem like a lot of work. And then probably if you fund it, over 15 years, depending upon the market, you might overfund it and, I don’t know. So it’s a little tricky, but the concept and strategy is just fine. But there’s limitations.

Joe: So yeah, he could fund his, his wife and then his daughter’s, and then if he wants to transfer or change beneficiaries from him to his daughter, if the daughter needs a little bit more cash, if not he can roll it. But the limitations, if he’s trying to use a creative Roth strategy, this is not the case for Chris. In 15 years, is he still gonna have income? And if he is, why wouldn’t you just directly contribute to the Roth or do the backdoor or do any other type of thing versus transferring the 529 plan because the transfer counts as a contribution. Just like Al said, you can’t like double dip or you can’t put the $35,000 all in at once. It’s a lifetime maximum contribution to the Roth of $35,000. That’s why I said it just kind of seems like now I got these other accounts that I gotta monitor and keep track of when potentially I can probably just make the contribution.

Al: Yeah, I mean, guess one advantage is you put the money in now and then it grows tax-free, and then so you have a higher amount to transfer, but still you’re limited to that currently $7500 a month. It’s now, it’s not even available current, you know, I think it’s 2024 maybe when this starts, but, yeah, I personally would not do it. I agree with Joe. I think it’s a bit too much effort for what it’s worth.

Joe: All right. Chris, congratulations on the little one. Maybe we get together and get the kids together and have a-

Andi: A play date. Awwww.

Joe: -little play date. It’ll be so much fun.

SECURE 2.0 is a circus and just for Midwestfabs – and everyone else that’s been asking about this new tax laws – we’ve got a brand new YMYW TV episode and brand new companion guide to prove it. Click the link in the description of today’s episode in your favorite podcast app to go to the show notes, watch the TV show, download the guide to the SECURE 2.0 Circus, and to see that picture of Midwestfabs’ walking companion, the very cute dog named Jake from State Farm. It’s all in the podcast show notes at YourMoneyYourWealth.com.

Will Municipal Bond Income Bump Me Into a Higher Tax Bracket? (Bobby, Philadelphia)

Joe: Got Bobby. Bobby from Philadelphia writes in. Philly. You ever been to Philly, Big Al?

Al: I have been to Philly, a couple times.

Joe: Yeah? Brotherly love? You like it?

Al: Yeah, I do like it. I saw, let’s see, the Liberty Bell and all the stuff there was, it was fun.

Joe: Okay, Bobby. “Thank you for the show. I learned a lot listening regularly on my daily commute. I’m 45 and live outside of Philadelphia with my wife and two little boys that are 7. We are pretty boring when it comes to cars, Chrysler Pacifica and a Honda Accord.” Yeah, that is pretty boring.

Al: If you don’t say so yourself huh?

Joe: “Drink of choice is a local brew, like Dogfish Head or 60 Minute Brewing-“ or is it Dogfish-

Andi: Dogfish Head 60 minute IPA. Yep.

Al: Oh, there it is.

Joe: So it’s all one word, Dogfish Head 60 Minute.

Andi: Well, Dogfish Head is the name of the company, and then the beer is called 60 Minute IPA.

Joe: Oh. Dogfish Head-

Al: So Andi’s got the picture up on the screen. It looks like it’s in a black bottle. I mean black label, with a black, little case carrier for the 6-pack.

Joe: Yeah. It’s Dogfish Head man. “Over the last 20 years, my wife and I have been using a buy and hold strategy to build an income portfolio held in our taxable accounts that will cover our expenses in retirement. In this way, we hope that our post-retirement income will continue to grow and keep pace with inflation without having to withdraw from our principle.” All right, so he is building an income strategy here, Al. He just wants to live off of interest and dividends. Don’t touch the principle and just hold onto this thing. “I expect the portfolio will generate $150,000 by the end of this year.” $150,000 of income. He’s 45 years old. How big of a portfolio do you think that is?

Al: That’s high. I mean, even with high dividend paying stocks, it’s gotta be up there. What do you get?

Joe: I don’t know. I mean, unless he’s going really crazy on the risk and trying to get like 7% to 10%, like, you know, dividends. Yeah. I mean dividend yields right now what, 3% or 4%? So that would be, what, $3,000,000 to $4,000,000?

Al: Yeah, exactly. So that’s the first comment is sometimes when you have a high income portfolio like that, that you may be taking on more risk than you realize.

Joe: Could be. I mean, if he’s got $5,000,000, then I think he’s in line. But if he’s got a lot less than that, it would be interesting to see what he’s doing. $150,000 but at- man, at 45. Good for him.

Al: Yeah, you bet.

Joe: “Got no debt. We’re fully funding 401(k)s, IRAs, 529 plans for the boys. I don’t know when exactly we’ll retire. But could be in the next few years. Our portfolio is comprised of a diversified group of 80% dividend growth stocks-“ Ooh, there it is- dividend growth stocks, not just dividend stocks, Big Al.

Al: Yeah. Dividend and growth.

Joe: Dividend growth stocks. “-20% individual municipal bonds. I invest myself because I enjoy it and because I believe I can mirror the results of the dividend fund.” So he can beat the manager. Bobby from Philly. He’s got the secret sauce.

Al: Maybe he has, if he can generate $150,000 of income.

Joe: He’s highly diversified, but he could get a better yield. All right. Good for you Bobby. “I only invest in stocks that have a long history of growing and stable dividends, and I limit exposure to any individual stock to less than 1% of the portfolio income. For the muni bond part of the portfolio, I only buy bonds rated A and above, and I only hold bonds through maturity to limit my interest rate risk. Part of the reason I invest in muni bonds is to limit income taxes when we decide to retire. I’m sure to keep my dividend portfolio of our income below $115,000, so my tax rate on qualified dividends will be 0%, and my tax rate on ordinary dividends will be around 22%.

My understanding is that $115,000 is the top of the income level where I can qualify for 0% tax on qualified dividends. This of course, includes the standard deduction for our family. Thanks for hanging in there if you got this far.” You’re welcome. Bobby. Guy’s just patting himself on the back all the way through this. “My actual question is about taxes.” Then why don’t you just ask it? You just gotta go through this diatribe of how great you are picking dividend stocks and you can beat managers. Yeah, I digress. I need blackfish tail 60 minute brew.

Al: You need a couple of those right now Joe.

Joe: I do. “Since muni bond income is not taxed at the federal level, I believe I should be able to stay in that 0% tax bracket for a qualified dividend income as long as my taxable income stays below that $115,000. Am I thinking about this correctly? Or could muni income contribute to taxable income and bump me up into a higher tax bracket? Thanks for the show, Bobby in Philly.” Thank you, Bobby. Great question. I really enjoy the question.

Andi: Even if it did make him cranky.

Joe: Didn’t make me cranky. Bobby from Philly, he gets it.

Al: Yeah. He, it’s just being human, right? Just having a conversation.

Joe: Yeah. He’s sitting around having his little Blackfish and he is like, yeah. And he is talking to his buddies about how great he is at picking stocks. Yeah. My portfolio- How’s your portfolio? Oh really? Mine’s gonna produce about $150,000 of dividend.

Al: Yeah. Yeah. What’s your dividend rate?

Joe: Yeah. What? Yeah, what’s your dividend yield?

Al: I don’t know, maybe a couple thousand. Well, mine’s $150,000.

Joe: You ever heard of the fund SCHD?

Al: I can do better than that.

Joe: I can do better than that. Alright, so he’s building a portfolio. So the, besides, all of that. He’s building a portfolio that he can live off of, but I don’t know why he’s doing it the way he’s doing it. And maybe we can get into that later. But let’s just answer the question is that, so he’s got municipal interest and sometime municipal interest could be an add back, you know, maybe, when it comes to calculating certain taxes.

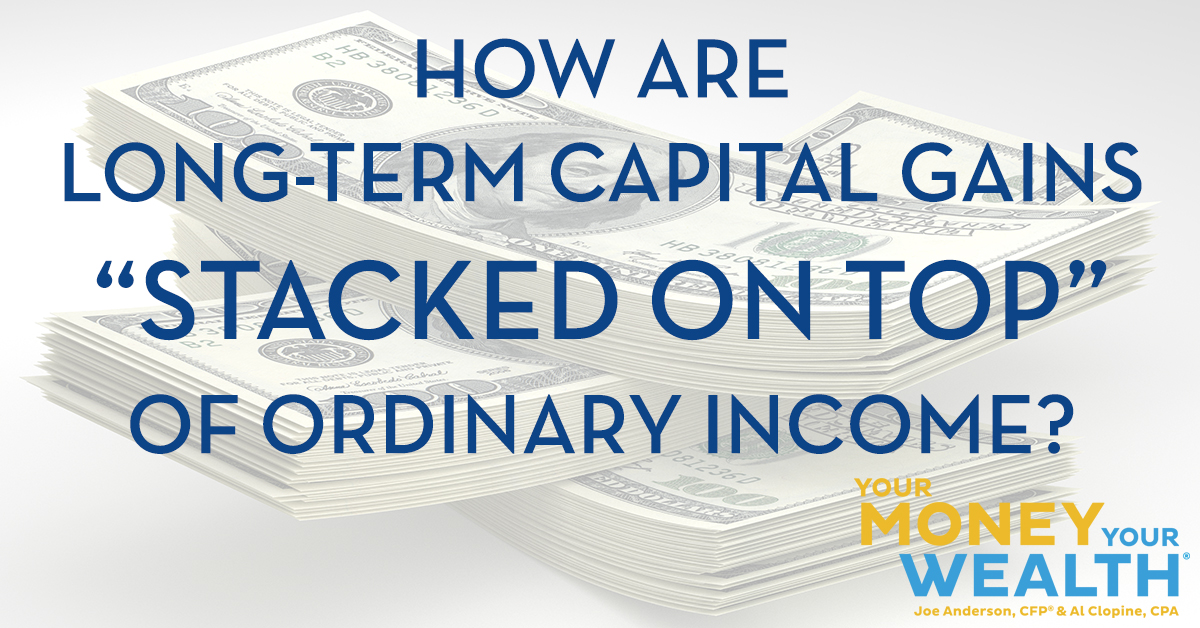

So he’s trying to stay in that 12% tax bracket. Because if you stay in the 12% tax bracket, then capital gains or qualified dividends fall into that 0% cap gain rate. So he doesn’t necessarily have to pay taxes on that. So if he has that municipal interest that could be pumping or, you know, added, let’s say another $10,000, does the capital gain sit on top of that? or is that not even included in the overall taxable income calculation?

Al: Yeah, great way to frame it, Joe. So municipal bond interest is not includable in your taxable income and you are right, it is includable for some modified adjusted gross income calculations. But not in this case, not for taxable income. So the way this works and, and there might still be a little confusion by Bobby, so let me kinda explain this. So what happens first is your ordinary income is kind of the first level, right? Any ordinary income that person has minus the standard deduction is kind of your base. And then capital gains sit on top of that. And as long as by the time you get to total taxable income and it’s below the- currently $115,000 because you subtract $25,000ish of standard deduction, you get about $90,000 of taxable income, which is the top of the 12% bracket. Then as long as all your income is capital gains, it is 100% tax-free or qualified dividends, 100% tax-free. To the extent that any of those are ordinary, so they would be taxed in the- if they’re above the, let’s say that standard deduction, they’d be taxed at the 10% rate or 12% rate.

Joe: Yeah, because you’re right, I was confused with that too because he’s like, my qualified dividends will be 0% and my tax rate on ordinary dividends will be around 22%.

Al: So I think he’s thinking, Joe, maybe that first he does capital gains that are 0% and then any other ordinary dividends get taxed at 22%. It’s actually a better answer than that.

Joe: Right. This is a good reminder for everyone that capital gains will always sit on top of ordinary income, not the other

way around.

Al: Yeah. So do your ordinary income first minus your standard deduction or itemized if you itemized. So you come up with whatever that is, you add your capital gains to that and all the way up to, in this case, after you’ve- actually $90,000 or taxable income, all those capital gains, as well as qualified dividends are taxed at 0%. Anything above that, if it’s capital gain or qualified dividend is taxed at 15%.

Joe: Right. So his qualified dividends would start first and then his qualified dividends would sit on top of that, is what you’re saying?

Al: Yeah. Ordinary income, ordinary dividends first minus standard deduction, and then capital gains and qualified dividends sit on top of that.

Joe: Got it. Okay.

Al: Yep. so that’s how that works. So probably instead of 22% for his ordinary dividends, it would probably be, I’m guessing, 10% or 15%, depending upon the level, unless there’s a lot of them. But I don’t think there are, because I think he said the total income’s $150,000.

Joe: Yeah. But then he wants, ‘our expected portfolio to generating $150,000 by the end of this year.’ But then he’s trying to control that to get it to $115,000. So it’d be interesting to see how he’s gonna do that if it’s – because he is so good- it’s just maybe more income than he needs.

Al: Well, he could do it with muni bonds, but that might reduce his rate of return. Or let’s see, he could switch to some growth stocks that don’t have the dividends, which, that’s a whole ‘nother discussion, which we don’t have time at this point to think of a total return rather than an income only return.

Joe: I think we’ve talked about that quite a bit on the show is that we love dividend paying stocks, don’t get me wrong, but, just having a sole strategy of just focusing only on high paying dividend stocks, to us could be a little short-sighted. You might be taking on a little bit more risk than you think. Or you can potentially create very similar income, but you create your own synthetic dividend like Warren Buffet, right? He never necessarily wanted to invest in, in dividend paying stocks because he didn’t want the company to force the dividend out where he would potentially have to pay tax on it. He would want to control his income by creating a synthetic dividend versus having the company distribute it.

Al: Yeah. And you do that by selling some of your shares and that it’s long-term capital gain, same impact, but you’re in more control. And one more further point, Joe, is the large growth

US companies have done very well the last 10 years. They’re also the highest priced. So based upon how you think about that, they could have a little more risk than other types of stocks. No one knows for sure, but that’s possible. And then dividend stocks, everyone’s been searching for dividend return, so I’ve gotta believe that dividend high US growth stocks are- they’re probably the highest price right now.

Joe: But he’s got it under control and he is doing a really good job. So, congratulations. I mean, if you really love this stuff and you enjoy it, and you watch it, by all means, go for it. From a tax perspective, I think he’s gonna be sitting in an even better spot than he thought.

Al: Agreed.

Joe: Thanks for the question, Bobby.

Can I Avoid Capital Gains By Investing Less Aggressively Over Time? (Joe, Aston, PA)

Joe: We got Joe from Aston PA. “Hi Big Al, new dad Joe, and amazing Andi.” Yeah, about a year and a half new, but who’s counting?

Al: That’s still new compared to me.

Joe: Yeah. Oh, geez. “I’ve been listening for many years and truly appreciate the continuous education you provide and the awesome humor derails. I drive a 2011 Honda CRV. CRV. Have a yorkie poodle named Guinness and drink all liquids. I appreciate the virtual invite, Big Al, to this nice bar in Hawaii to do some spit balling with you guys.”

Al: I’m here right now.

Joe: I know you are.

Al: What island are you on?

Joe: Let’s see. The mai tais are getting to me, so I hope this capital gains question makes sense.” You got a Mai tai yet, Big Al today?

Al: Uh, no. No, no. In fact, I’ve been here, this is the third day. I haven’t had a drink since I’ve been here.

Joe: Well, what is wrong with you?

Andi: Yeah, really.

Al: I’m just, you know, taking a break.

Andi: Trying to make sure you can answer the questions.

Joe: Well, I mean, what you were in New Zealand for a month, so you have a lot of New Zealand ale.

Al: I did. Alright, so this is a little- little reset.

Joe: Yeah, I got it. You know. After a vacation you need- you need a vacation from your vacation.

Al: You do. That’s right.

Joe: Yeah. I know who you’re with. So I would imagine there was a few cocktails that went down.

Al: You know, at least two of the people I’m with and so, yeah. You have a pretty good idea.

Joe: Yeah, I have a really good idea. Alright. Okay, so let’s, and let’s get uh, back to the Mai tais, here. “Situation, someone has aggressive 401(k) investment mix, 90/10 stock/bonds, for 30 years, and then sells most of the stock mutual funds and moves the balance into bond funds within the 401(k). If the rebalance is now 20/80 stock/bond, and will remain this way for two years prior to retirement, do those 30 years of mutual fund capital gains ever get paid to the government as taxes? Is this a legitimate strategy to avoid years of capital gains taxes if you plan to become less aggressive in retirement anyway? The company has never passed along extra fees to employees, but this seems to be a tax due to the individual. With a balance of several million dollars, this could be significant savings when one starts withdrawing in a few years. Maybe this leads to a general question on how capital gains taxes are paid from 401(k) accounts. Is it only when they are sold and taken as withdrawals, not sales within the 401(k)plan? I hope this question makes sense. My head is spinning from the drinks. No idea how Al slams Mai tais and provides financial spit balling. Have a great summer gang. I had the money outside of my 401(k) but wanted to simplify my question. I hope. Thanks as always for taking the time to educate us.” Yeah, he’s had way too many Mai tais.

Al: A couple too many. Missing one basic fact here, so yeah. So when you buy and sell within a 401(k), there’s no current taxation, right? So no capital gain tax to pay. However, when you withdraw the money, it’s taxed at ordinary income. So what could have been a cheaper tax if it was held outside a retirement account is taxed 100% at ordinary income, which by the way, every time you take $1 out, you pay ordinary income tax rates. And by the time you’re currently 73, you have to take the money out because of required minimum distributions. So yes, the government will get their money, they’ll get more than they would otherwise get because it’s not capital gain, it’s ordinary income. It’s a much higher tax. So, the only benefit is you can rebalance inside a 401(k) and not pay current tax. But believe me, you’re gonna pay a lot of tax as you pull the money

out.

Joe: Everything is tax-deferred in a 401(k) account. So you start with $10, it grows to $10,000,000. There is no tax on that growth until you start taking distributions from the overall account. If it’s outside of the retirement account, well then that’s when you have capital gains tax. So let’s say if you’re rebalancing along the way, you could have capital gains, you could have capital losses. So you’re investing in a brokerage account, it’s completely different from a tax perspective on how you want to be looking at that on an annual basis than if it in a 401(k) plan. Because it’s a set it and forget it for a 401(k), or you could trade all day long, you could day trade the hell out of it, and you’re not gonna have any type of tax advantage whatsoever within the overall account. You’re getting the tax deferment, there is no tax at all until you take the distributions.

That’s when you’re taxed at ordinary income rates. Most people are in a lower tax bracket in retirement. Most. I’m not saying you are, and not saying most of our listeners are probably in a different tax bracket in retirement. It’s probably higher. Because they’re listening to this podcast because they’re interested in financial education and they’re doing things about their overall financial life. Most people don’t necessarily save. And so when the 401(k) plan was, I guess born in 1974, the top marginal rates were in the high seventies, mid seventies. The top marginal rate in the history of the tax code was in 90%. Right now it’s almost at its lowest, so there is no taxation along the way, but when you pull the money out, you will be taxed. And so you might be in a lower bracket or you could be in a higher tax bracket. So you just wanna understand the taxes as you are building and accumulating wealth and then creating the income. Thanks for the question, Joe. Keep drinking those Mai tais, brother.

Pros and Cons of Selling a Rental House Right Now (Joe, Chula Vista)

Joe: Joe from Chula Vista writes in. “We are seniors, 73 and 80, with a 55-year-old son who is single. We are debt free. Have 3 rental houses in Arizona. We’d like to know the pros and cons of selling the rental houses now. All houses are paid for. We are thinking to unload them because of our age. Thanks.” Why would they unload? Just the probably- they don’t want to have the maintenance of it?

Al: Yeah, I think so too. I mean, I get it. You wanna simplify when you get older. From a tax standpoint, you’re actually a little better off if you hold them until you pass because your son will get a full step-up in basis and can sell them with no taxes. But that may not be a realistic, maybe you don’t wanna manage, maybe you can have your son manage them. If he’s gonna inherit them anyway. Maybe he would be motivated to save the taxes. If he doesn’t want to and you really don’t want them, yeah. You can sell-

Joe: You can hire a property manager.

Al: Yeah. You hire property manager. But if you still wanna sell because you wanna simplify, you don’t wanna deal with it anymore. I would understand that. You’re just gonna have to pay capital gain taxes on the gain on sale plus the depreciation recapture. So the taxes will be probably higher than you’re expecting.

Joe: Yeah. So then the son that is gonna inherit it all will probably get less. So if you want the son to get more- but if the son needs it now- he’s 54 and single. I don’t know. Does he need the cash now or can he wait another, you know, 10, 15 years, whatever?

Al: Yeah. or on the other hand, maybe one out of the 3 is more of a problem than the other two. You sell that one to get rid of it and have a property manager or your son manage the other two so you don’t have to think about it. That’s what I’d probably do.

Joe: Alright, thanks for the question, Joe.

How capital gains tax and ordinary income tax work, and the best strategies to manage them, are regular topics here at YMYW. Podcast episode #325 compiles many of those discussions for cap gains vs. ordinary income tax explained all in one episode. Click the link in the description of today’s episode in your favorite podcast app to go to the show notes and find episode 325 in the big fat list of free financial resources, right before the transcript of the episode. And if you want Joe and Big Al to spitball your plan for your retirement, taxes, and overall finances, just click Ask Joe & Big Al On Air there in the show notes and send them on in as a priority voice message or as an email.

An Easy Breezy Self-Employed Retirement Account Better than the SEP IRA? (Steve, Las Vegas)

Joe: We got Steve from Las Vegas writes his deposition again, Big Al.

Al: The way he writes it kinda looks like it’s a deposition. Kinda expect an attorney’s signature at the bottom.

Joe: Very, very formal here. “My daughter and son-in-law need an easy breezy retirement account to put away some self-employment income. I told them to check with a local bank, re a SEP IRA. I see that my discount broker also offers SEP IRA accounts. Is there something better than the SEP IRA for them? The idea is a retirement plan that is cheap and quick to set up and maintain no employees, IRS Schedule C. PS. Is there a show about SEP IRAs in the YMYW show archives? I looked and I couldn’t find anything. I listen to YMYW online on News Radio AM 600 KOGO San Diego. I drink a tall glass of water and I use public transportation. Love the program. Steve.”

Andi: So I don’t have a full episode that’s about the SEP IRA. There’s questions about it all throughout. So, you know, maybe we’ll need to do a compilation episode at some point all about the SEP.

Joe: Don’t we have like a- we have a TV show on retirement accounts.

Al: Yeah.

Joe: Then we have like- don’t we have like a white paper on all the different retirement accounts too?

Andi: There’s a white paper that’s on all the different types of IRAs. And I think we actually have a blog post about self-employed small business owners, different options for retirement accounts.

Joe: Huh. Okay.

Andi: So I will link to all of that stuff in the show notes.

Joe: Got it.

Al: Perfect.

Joe: He needs a solo 401(k).

Al: That’s the best. It basically, it’s the same contribution amounts as a SEP IRA for the employer part. But the employee part, you don’t get in in the SEP, but you do get into solo 401(k). So you can put a lot more away with a solo 401(k). I would say Joe from simplicity, they’re both very simple. There’s one the little extra nuance with a solo 401(k) in that you actually have to have a plan document. But the brokerage houses have them already made, so you get kind of an off the shelf one. It’s super easy and you do have to close it out when you’re done with it. But, besides that, yeah, that’s usually what we recommend for the main reason that you can put a lot more in it if you want to.

Joe: Yeah. Solo 401(k), just Google that. Most of the discount brokers have the solo 401(k), because you get the employee and the employer. Because, the son-in-law and daughter are the employer and employee. Because they’re self-employed so they can kind of get both sides of the table here.

Al: And it has to- you have to have no employees, which they have, let’s just say they- just an easy example. They make $40,000 of income. So with a SEP IRA they could do 25%, so they could put $10,000 away. With a solo 401(k), they could also put $10,000 away for the employer part, but they could put $22,500 for the employee part. Which if they don’t necessarily need the tax deduction, they could put that in a Roth, which is a great thing, particularly if they’re young for growth. If they need to live off of, if those amounts are just too high, then you can keep with a SEP, because it’s super simple. But when you want it, when at the point where they wanna put more away than just the 25% of the profits, then yeah, definitely go solo 401(k).

Joe: All right, Steve. Hang out. Have fun on that public transportation there in Vegas with that cold glass of water. This is the end of the show?

Andi: That’s the end of the show.

Joe: This is it. We’re done. Well, wow, time flies when you’re having fun. Alright, that’s it for us. We’ll see y’all next week. The show’s called Your Money, Your Wealth®.

Andi: Find those links to both the blog on Small Business Tax Strategies and the Ultimate IRA Guide in the podcast show notes. Got a quick comparison of fridges in the basement vs. the garage in the Derails at the end of the episode, so stick around. Help new listeners find YMYW by telling your friends about the show, and by leaving your honest reviews and ratings for Your Money, Your Wealth in Apple Podcasts, and any other podcast app that accepts them like Amazon, Audible, Castbox, Goodpods, Pandora PlayerFM, Podcast Addict, Podchaser, Podknife, Spotify, and Stitcher.

The Derails

_______

Listen to the YMYW podcast:

Amazon Music

AntennaPod

Anytime Player

Apple Podcasts

Audible

Castbox

Castro

Curiocaster

Fountain

Goodpods

iHeartRadio

iVoox

Luminary

Overcast

Player FM

Pocket Casts

Podbean

Podcast Addict

Podcast Index

Podcast Guru

Podcast Republic

Podchaser

Podfriend

PodHero

podStation

Podverse

Podvine

Radio Public

Rephonic

Sonnet

Spotify

Subscribe on Android

Subscribe by Email

RSS feed

YouTube Music

IMPORTANT DISCLOSURES:

Pure Financial Advisors is a registered investment advisor. This show does not intend to provide personalized investment advice through this broadcast and does not represent that the securities or services discussed are suitable for any investor. Investors are advised not to rely on any information contained in the broadcast in the process of making a full and informed investment decision.

• Investment Advisory and Financial Planning Services are offered through Pure Financial Advisors, LLC, a Registered Investment Advisor.

• Pure Financial Advisors LLC does not offer tax or legal advice. Consult with your tax advisor or attorney regarding specific situations.

• Opinions expressed are not intended as investment advice or to predict future performance.

• Past performance does not guarantee future results.

• Investing involves risk including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

• All information is believed to be from reliable sources; however, we make no representation as to its completeness or accuracy.

• Intended for educational purposes only and are not intended as individualized advice or a guarantee that you will achieve a desired result. Before implementing any strategies discussed you should consult your tax and financial advisors.

CFP® – The CERTIFIED FINANCIAL PLANNER™ certification is by the Certified Financial Planner Board of Standards, Inc. To attain the right to use the CFP® designation, an individual must satisfactorily fulfill education, experience and ethics requirements as well as pass a comprehensive exam. Thirty hours of continuing education is required every two years to maintain the designation.

AIF® – Accredited Investment Fiduciary designation is administered by the Center for Fiduciary Studies fi360. To receive the AIF Designation, an individual must meet prerequisite criteria, complete a training program, and pass a comprehensive examination. Six hours of continuing education is required annually to maintain the designation.

CPA – Certified Public Accountant is a license set by the American Institute of Certified Public Accountants and administered by the National Association of State Boards of Accountancy. Eligibility to sit for the Uniform CPA Exam is determined by individual State Boards of Accountancy. Typically, the requirement is a U.S. bachelor’s degree which includes a minimum number of qualifying credit hours in accounting and business administration with an additional one-year study. All CPA candidates must pass the Uniform CPA Examination to qualify for a CPA certificate and license (i.e., permit to practice) to practice public accounting. CPAs are required to take continuing education courses to renew their license, and most states require CPAs to complete an ethics course during every renewal period.