Backdoor Roth IRA withdrawal rules and the mechanics of the mega backdoor (dump truck!) Roth. Can you still contribute to a Roth after a rollover? How do you calculate Roth conversion taxes due to the pro-rata rule? Also, how to calculate your retirement number for a long retirement or by age; a radical portfolio rebalance; why basis, gains, and losses are tracked; and donating stock upon death. Plus, does your financial advisor’s location matter?

Subscribe to the YMYW newsletter

FOLLOW US: YouTube | Facebook | Twitter | LinkedIn

Show Notes

- (00:55) Backdoor Roth IRA Withdrawal Rules (David)

- (04:53) Mega Backdoor Roth: How Long to Wait to Convert After-Tax 401(k) Contributions to Roth to Avoid 6% Excise Penalty? (Eric, Las Vegas, NV)

- (11:43) Can I Still Contribute to Roth Even Though I Did a Rollover? (Jim, Santa Cruz)

- (13:07) How Do I Calculate Roth Conversion Taxes Due to the Pro-Rata Rule? (Johnny G)

- (15:37) Radical Rebalance: Reallocating Dad’s Portfolio (Craig, Chicago)

- (19:47) How Should I Calculate for a Long Retirement? (Mick, San Diego)

- (21:46) Calculating a Retirement Number for a Certain Age (Will)

- (27:28) Why Track Basis, Gains, and Losses? (Perry, Jersey)

- (33:43) Donating Stock Upon Death (Tom, Chicago)

- (37:52) Does My Financial Advisor’s Location Matter? (Tom, Chicago)

Free resources:

Listen to today’s podcast episode on YouTube:

Transcription

Today on Your Money, Your Wealth® podcast #308, the fellas are pulled back into talking about Roth conversions – specifically, the backdoor Roth IRA – its withdrawal rules for David, and the mechanics of the Mega backdoor Roth – or dump truck Roth – for Eric! Plus, can Jim still contribute to a Roth even though he did a rollover? How does Johnny G calculate Roth conversion taxes due to the pro-rata rule? Also, calculating retirement numbers for a long retirement or by age for Mick and Will, a radical portfolio rebalance for Craig’s Dad, and the fellas explain for Perry in Jersey why basis, gains and losses are tracked. Finally, how much does your financial advisor’s location matter? The fellas answer that question for Tom in Chicago, along with a discussion about donating stock upon death. I’m producer Andi Last, and here are the hosts of Your Money, Your Wealth®, Joe Anderson, CFP® and Big Al Clopine, CPA.

Backdoor Roth IRA Withdrawal Rules

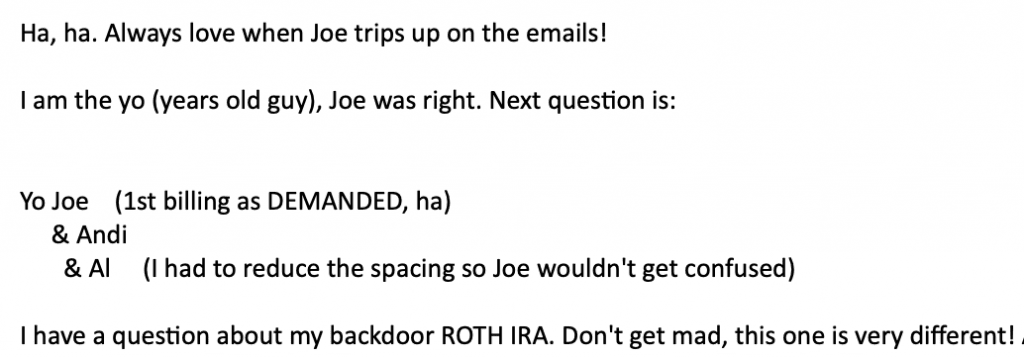

Joe: David writes in Alan, “Haha, I always love when Joe trips up on the emails.” What the-

Al: That’s never happened.

Joe: “I’m the yo, the years-old guy.” Remember that?

Al: Yeah, I do.

Joe: “Joe was right.” I know I was right. I don’t know what I’m right about.

Andi: That yo meant years old.

Al: You knew what yo meant.

Andi: And that he was the yo guy.

Joe: What’s up yo?

Andi: Like the 3rd time he’s emailed us.

Joe: Yo. What up yo? “The next question is yo Joe. First billing as demanded. Ha.” He’s a very Ha Ha kind of guy. Right?

Al: He is. Yeah. He’s one of those guys that likes to laugh at his own jokes. Yeah.

Joe: He loves it. “And Andi. HaHa.” Ok. “And Al. I had to reduce the spacing so Joe wouldn’t get confused.”

Al: He put us on 3 different lines.

Joe: Got it. I understand now.

Al: And indents for Andi, and even further indents for me.

Joe: There ya go. “I have a question about my backdoor Roth IRA. Don’t get mad. This one is very different, although you’ll probably rant about how every question is the same. I’m confused on withdrawing my contributions for my Roth IRA for my exact situation. I’m using after-tax money from my paycheck and contributing to an IRA. I then select not to withhold taxes and use that back doggy door to convert it into a Roth IRA. I am 35 and started this in 2019. Can I pull out my contribution if I have an emergency?” Non-deductible IRA contributions, he converts them into a Roth IRA. You will have access to those dollars, David, after 5 years. Because it is a conversion into a Roth, then you have full access to the converted dollars any time once you- what, he started that in 2019. So 2024.

Al: Yeah. And that’s a good point because a backdoor Roth is different than a Roth contribution. A Roth contribution, when you put the money in, you could withdraw at the next day. No harm, no foul, no penalty. As long as you’re not taking out any growth and income. But a backdoor Roth is actually a Roth IRA conversion that you convert. It’s a conversion, which means if you’re under 59 and a half, you have to wait 5 years for every single conversion to have access to the principal on the conversion. Call it the $6000, for example. And you’d have to wait till 59 and a half to pull out the income and growth.

Joe: “I’m trying to do this to reduce my cash emergency fund. I’m currently sitting on 6 months of expenses, including 2 rental property expenses. It is very unlikely 2 renters would stop paying it once. So I’m thinking I can present the Roth IRA contribution money to my big boss, my wife, as a last resort emergency money. Thank you for all the open discussion and laughs.” The big boss.

Al: Yeah. Yeah.

Joe: I don’t have a big boss.

Al: I thought you did.

Joe: I’m my own big boss.

Al: I thought you’re working on it.

Joe: Oh boy. I don’t know. Just do your own thing. David, you don’t need to ask the big boss. Just do it.

Andi: This is why you don’t have one, Joe.

Joe: This is what happens. That’s my advice.

Al: There you go.

Joe: No, it’s not an emergency fund. Because you’ve got to wait 5 years. So sorry to burst your bubble, but I would still look at doing it. You got 2- well, the likelihood of 2 renters blowing out? Yeah, ask Alan about that some other time.

Al: It happens.

Mega Backdoor Roth: How Long to Wait to Convert After-Tax 401(k) Contributions to Roth to Avoid 6% Excise Penalty?

Joe: We got Eric from Las Vegas, Nevada. “Hey, guys and Andi, I’m getting mixed signals regarding the mega backdoor Roth conversion strategy. Sorry. Please clarify, how long should I wait to convert the after-tax contributions in my 401(k), to either my Roth 401(k) or my Roth IRA, to avoid the 6% excise tax penalty?” Eh boy, Eric from Las Vegas is reading all sorts of stuff.

Al: You’re mixing and matching things.

Joe: You got mixed signals. Yes. Your signals are all tune in Tokyo. Come on, Eric. All right. Let’s- a couple of things. A backdoor Roth conversion- once again, he’s doing the mega backdoor-

Al: This is the mega. This is where you do it through the 401(k).

Joe: I think people don’t even know what the hell the mega backdoor Roth is. There are not that many plans that allow after-tax contributions. If Eric, you have a 401(k) plan that allows after-tax contributions, so you made after-tax contributions, you take those after-tax contributions from your 401(k), convert those after-tax contributions into a Roth IRA. That is called a conversion. There would be no tax. Why people call this stupid thing the mega backdoor, barn door, doggy door, whatever door, is that it’s more than you can put in as a regular contribution, right?

Al: Yeah, that’s right. A regular contribution is $6000 and a backdoor Roth contribution is you contribute $6000 to an IRA and then you convert that. And that’s all you can do. Now when it comes to 401(k), you have money withheld from your paycheck. You generally get a deduction on your pay. You pay less taxes. But when you fill that thing up, $19,500- some plans, not many, but some plans allow you to put more money in, after-tax money, money that you’ve already paid tax on. So that’s what we’re talking about. If your plan allows that and you put the money in, then you can turn around and take that money and convert it to a Roth. So now all the future growth in that after-tax part is tax-free.

Joe: The 6% excise tax is when you just dump a bunch of money into a Roth-

Al: – that you shouldn’t have. It’s like, wait a minute, I want to do a dump truck Roth. I’m going to take my $200,000 brokerage account. Let’s put that in the Roth. How’d you get that? I don’t know. I just wanted to. You talked about a mega, let’s do a dump truck one.

Joe: So I got $200,000 laying around. I thought I’d just put it into a Roth IRA. I listen to this show called Your Money, Your Wealth®. That’s all they talk about is mega backdoor Roths.

Al: So the thing is, you can only put money into Roth when you are allowed to. There are certain ways.

Joe: There are rules.

Al: There’s a contribution. Or a conversion. Those are- you can’t just do it. And if you put money to Roth that you shouldn’t, then you get the 6% and sometimes this happens to well-meaning people. They put $6000 into a Roth. And lo and behold, by year-end, they make too much money to qualify. So the IRS says till October 15th of the following year, you could pull the money out without paying the excise tax. But if you go past October 15th, you’ve got to pay that 6% tax each and every year that you keep that Roth amount in there that you weren’t allowed to contribute.

Joe: So right now, the- for 2021 Al, the income limitation for Roth IRA contributions is what?

Al: It’s $6000.

Joe: No, no, no. Income.

Al: Oh, income. OK, let’s see. For single it is-

Joe: $137,000? $147,000?

Al: I gotta find it. Between $125,000 and $140,000.

Joe: $125,000 to $140,000. All right. So if you make over $140,000, if you’re single Eric, then you don’t qualify for a Roth IRA contribution, which is only $6000, or $7000 if you’re over 50. That’s the max amount you can put into a Roth IRA as a contribution. If you make more than that, then that’s where the backdoor stuff comes into play, because there is no income limitation to put money into a regular IRA. So you put your $6000 or $7000 into an IRA. Because you make $140,000 plus or $200,000 plus as a married person, you can’t take the tax deduction. So now you have after-tax basis in the IRA, then you convert that into a Roth IRA. There’s basis. So there’s no double tax, there’s no tax, you never got a deduction. So there’s no tax on the conversion. So now the money is sitting in the Roth, but you can only do that with $7000. Or if you have a 401(k) plan that we talked about earlier that allows after-tax contributions, those after-tax contributions can be converted. But double-check, because it doesn’t sound like he has an after-tax component. That’s the biggest key to the mega backdoor.

Al: Yeah. You have to have that. Otherwise, forget about it.

Joe: Yes. And most employers don’t allow- don’t have it. So if you’re just throwing cash above $6000 from your brokerage account into a Roth, then that’s where the excise tax comes from.

Al: I happen to know of a larger payroll company that does 401(k) plans that never even heard of after-tax contributions. And they’re in the business, so just be careful of all this.

Joe: So, Eric, hopefully, that helps. Because there’s no 6% excise tax penalty.

Al: That’s only if you put money into something that you shouldn’t have. Another example would be you contribute to an IRA or a Roth IRA and you don’t have any earned income and your spouse has no earned income. Then you didn’t qualify. So you put money in that you shouldn’t have. And so that’s where the 6% excise tax goes- comes into play each and every year you leave it in. So let’s say you do that- $6000 goes into the account and you leave it there for 10 years. And it never grew. 6% over 10 years. That would be, what, $3600, that would be your excise tax. And if it’s 20 years, your penalty is more than your account.

Joe: Right.

Can I Still Contribute to Roth Even Though I Did a Rollover?

Joe: “Hello Joe, Andi, and Big Al. Jim from Santa Cruz calling.” He’s got a question that does not involve a Roth conversion. “I hope this makes Joe very happy! In the first half of 2020, $2000 of payroll deductions were deposited into my workplace 401(k) account. I left that company in July. In August I rolled those contributions into a personal Roth IRA. I’m 60 years old. Am I still allowed to make a full $7000 contribution on my Roth account for tax year 2020? Or did the rollover contributions count against the $7000 yearly maximum? Thanks as always for the great show. Jim from Santa Cruz.” It’s a good question, Jim.

Al: It’s a great question because it’s very confusing for a lot of people.

Joe: Yeah. He put $2000 into his Roth 401(k), left the company, rolled the $2000 from the Roth 401(k) into the Roth IRA.

Al: Yes. So does that count as part of your contribution?

Joe: The answer is No. You are good to go. You can still contribute the full $7000 into the Roth IRA.

Al: So a couple of things. If you put money into a Roth 401(k), that does not affect your Roth contribution. And if you do a rollover from your 401(k) Roth into a Roth, that does not count either. So you’re good either way.

How Do I Calculate Roth Conversion Taxes Due to the Pro-Rata Rule?

Joe: Johnny G writes in. “Hello Joe, Big Al, and Andi, writing back in. I’m 27 and started my new business last year and not paying myself much this year so I’ll be in the 12% tax bracket. I have one of your favorite questions, Roth and the pro-rata rule. I have a 401(k) and my Roth IRA and should be about $30,000 in my simple IRA by the time the 2-year mark comes due. While in this low tax bracket, would it be prudent to convert $30,000 in simple over to my Roth? I know you all suggest having money in different tax buckets, but I have many more years to save into the pre-tax. It seems like it could be a good idea to get more money into a tax-free bucket while in a low rate. If I should convert, how do I calculate the taxes I owe due to the pro-rata rule? You all rock. Keep up the great work. Johnny G.” Johnny G.

Al: Family dog.

Joe: All right. Yeah. Convert. Convert.

Al: Yeah for sure. Low tax bracket. You’re young, that makes 100% sense. And the pro-rata rule doesn’t apply. It’s all fully taxable.

Joe: Correct. So you would pay 12%- well I would need to know what your taxable income is.

Al: Yeah. So it depends on what bracket it puts you in. So some of it, maybe all, will be taxed in the 12% bracket, but some may be taxed more because it may push you into a higher bracket. You might want to do some this year, some next year.

Joe: Yeah for sure. If you have a higher tax year though next year, maybe you just do less. But yeah, you want to- at the 12% tax bracket at 27 years old that thing will compound tax-free. I think that be pretty powerful.

Stick around to the very end of today’s episode to hear the giant Derail about Johnny G’s dog Maverick. And hey, David, Eric, Jim, Johnny G, and everyone else asking about Roth contributions and conversions, this is your call to download The Ultimate Guide to Roth IRAs for free from the podcast show notes at YourMoneyYourWealth.com. It explains in depth what a Roth IRA is and how you can benefit from having one, how a Roth IRA differs from a traditional IRA and from a Roth 401(k), the rules for contributing to a Roth, Roth conversions and backdoor Roth conversions, the rules for taking withdrawals from your Roth account, and more. Click the link in the description of today’s episode in your podcast app to go to the show notes to download your Ultimate Guide to Roth IRAs for free, and of course, if you still have questions, you can click the Ask Joe and Al On Air banner there in the show notes and send them in. Continuing now with your non-Roth questions.

Radical Rebalance: Reallocating Dad’s Portfolio

Joe: Craig from Chicago writes in “You’ll be glad to know that the word, Roth-” oh, he put it-

Al: – like a swear word.

Andi: – like it’s a bad word.

Joe: “- is nowhere in this question.” Thanks, Craig.

Al: Craig, we like you already.

Joe: Craig. Love you buddy. Not that I don’t love the Roth IRA and the conversions and the backdoor and the super backdoor, just really tired of talking about it.

Al: How many years have we talked about that?

Joe: It’s about 15. “I took over my father’s finances from a friend broker- of his who- my dad and was in questionable investments, MLPs, non-traded, etc.-” So. OK. He’s taking over the family finances. I guess he looked at his dad’s brokerage account. He’s got some questionable investment choices in there. “It’s going to be difficult to get out of these so I’m dealing with the IRA and brokerage accounts first. The IRA is manageable as I can get out of those bad risky investments without the tax consequences, right?” Yes. Anything inside a retirement account you’re good to go. You can buy, sell, trade, day-trade, do whatever in the retirement accounts, IRAs, Roth IRAs, whatever because they grow tax-deferred. Just make sure that you’re doing it correctly as you transfer that money into another IRA that you’re not taking distributions. We’ve seen that in the past. “So my plan there is just to rebalance to the 3-fund portfolio 60/40.” Three fund portfolio- I think it’s like Vanguard Total Stock Market Index, total international index, and a bond fund?

Al: That’s exactly what he’s referring to.

Joe: OK.

Al: Or Fidelity or whoever. It doesn’t matter. Which is not a bad, very simple way to go.

Joe: I agree. “But the brokerage account is large and 90% invested in individual stocks. I’d like to sell the bulk of the stocks and rebalance into Fidelity, no-fee mutual funds ending up at a 60/40 split. But I understand that he will have to pay taxes, at least 15%, on any gains. Do I understand this right? And is there some strategy to lessen the tax impact of a radical rebalance like this? I drive a Tesla. Thanks.”

Al: That’s good.

Joe: Yes. Tax-loss harvesting comes to mind. But make sure that you’re rebalancing just- I guess- if you’re going to take over the family finances you don’t want to blow them up in taxes, just to make your life easier. He’s got good investments. Keep the ones that are good and then get rid of the ones that are bad.

Al: I think that the way I would think about it is that some of the individual stocks probably that have a bunch of gains, maybe you use those as proxies for an S&P 500 Fund, which is not ideal. I understand it’s not as diversified as you would like. But if it avoids causing a whole bunch of taxation. We don’t know how old your dad is. And right now under current law when someone passes away the next generation gets a full step-up in basis so there is no tax problem. So if your dad is 70 and his dad lived to 95 then that’s probably not going to be a great strategy. On the other hand, if your dad’s like my dad who’s 87, you hate to think about it but-

Joe: Wow. Morbid.

Al: – we don’t live forever. And even he said it, I don’t know if I want to get to 90.

Joe: So yeah Craig, if your dad’s a-tippin’ the toe…

Andi: What does that mean!?

Al: Well, I gotta be realistic here, right?

Joe: Yeah. If he can barely fog a mirror, then don’t do anything. Just hold on.

Al: Otherwise, do your best. Just create some proxies on some of these stocks and try to backfill the best you can.

Joe: Yes. Hopefully, that helps. But you know we’ve seen that in the past. Like- I’m taking over the family finances, dad’s 90 and all of a sudden they’re selling all this stuff and capital gains happens and they re-balance it. But then the old man dies like a couple of weeks later, they could have got a full step-up in basis, no taxes due.

Al: Or mom’s about to pass away, she sells all her real estate so it’s simpler for the kids and pays a bunch of tax that they wouldn’t have paid.

How Should I Calculate for a Long Retirement?

Joe: I got an email here from Mick from San Diego. “Hey, guys. How much do you change your calculation for retirement savings if you expect to be retired for a long time? For example, retired at 50, wife and I are the same age, very good health, no kids, modest home in Southern Cal worth about $1,000,000, no mortgage, $7,000,000 in savings, 60% stock, 40% bonds, budget $170,000 a year. Can we do this? Adjusted for inflation until we die at age 100?” The numbers look pretty good.

Al: The answer is yes. So here’s the math, you take the $170,000 a year that you need, divide that into $7,000,000. And you look at your distribution rate. Which I did that calculation, 2.4%.

Joe: Ok.

Al: So what I would say, Joe, that the change in the calculation for retirement spending is when you retire younger, it should be something less than 4%.

Joe: It should be 3%.

Al: It should be 3%, 2.5% maybe. 2.5% or 3%, retiring at 50. And this is 2.4%. So this passes our very simple, quick, easy test. Now, you still have to do a lot right. Because this money has gotta last for 50 years.

Joe: Right. It could blow up on them. It’s close. It’s super close. Because he wants to spend $170,000 a year, but he’s got no mortgage and he has $7,000,000. So one year if he gotta spend $150,000 max-

Al: – dial it back a little bit.

Joe: Can he dial it back, bro?

Al: And Social Security will eventually kick in. So there will be that. So yeah, I think it sounds good, but when we say you’re probably Ok because you’ve got a 2.4% distribution rate, you’ve got to invest properly for 50 years. So it’s like this isn’t the slam dunk. It looks good on paper, but you got to do a lot of things right.

Calculating a Retirement Number for a Certain Age

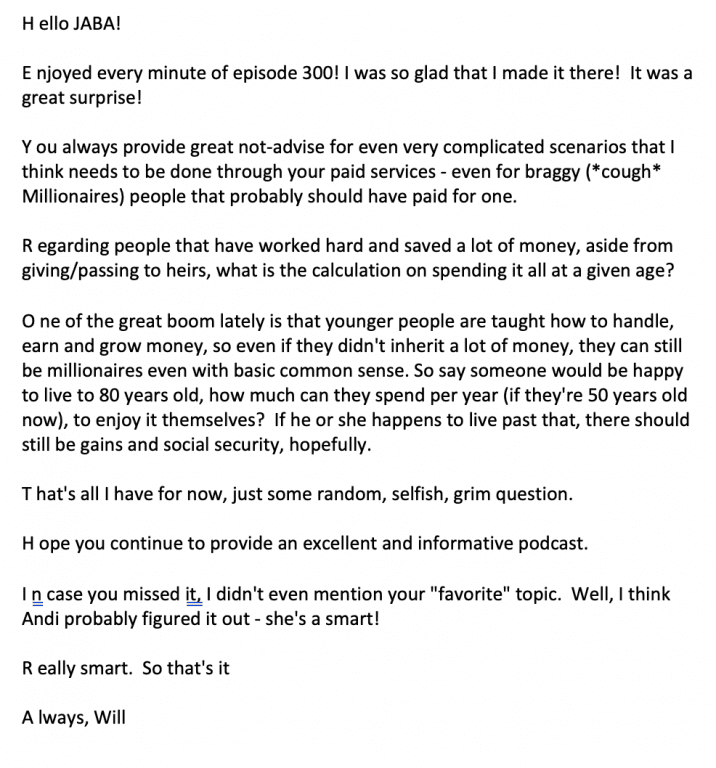

“Hello JABA.” Jaba the Hutt. I would say what Joe- what?

Al: Joe, Andi and Big Al.

Joe: Joe, Andi, Big Al. JABA.

Al: JABA.

Joe: Jaba the Hutt?

Al: Yeah right.

Joe: A lot of Star Wars references-

Al: There sure are.

Joe: “Hello- ”

Al: You like Darth Vader. That’s your favorite.

Joe: All of them. Big fan of Star Wars.

Al: I still think you might have been Chewbacca in some of the episodes.

Joe: Could have been.

Al: I’ve heard you make the sound just like him.

Joe: Can’t make it today. These novels are killing me. These- you know- everyone’s kind of taking advantage of us, Al. “Enjoyed every minute of episode 300. I was so glad that I made the cut. It was a great surprise. Always provide great not-advice for even complicated scenarios that I think needs to be done through your paid services, even for braggy cough-cough millionaires, people that probably should have paid for one.” Thanks, Will. He’s right. All these people just grinding us Al, for free advice.

Al: Right.

Joe: “Regarding people that have worked hard and saved a lot of money aside from giving/passing to their heirs, what is the calculation on spending it all at a given age? One of the great booms lately is that younger people are taught

how to handle, earn, and grow money. So even if they didn’t inherit a lot of money they can still be millionaires even with basic common sense. So say someone would be happy to live to 80 years old, how much can they spend per year if they’re 50 years old now, to enjoy it themselves?” I feel like I’m reading like a haiku or something.

Al: You are.

Joe: “If he or she happens to live past that, there should still be gain in Social Security hopefully. That’s all I have for now just some random, selfish, grim question. Hope you continue to provide an excellent informative podcast. In case you missed it, I didn’t even mention your favorite topic. Well I think Andi probably figured it out. She’s so smart. Really smart. So that is.”

Al: That’s it. “Always. Will.”

Joe: “So that is. That’s it. So that’s it.

Al: That’s it. That’s it. That’s all folks. Well, so it turns out that the first letter of every paragraph, it says Hey Roth IRA.

Andi: So Hello JABA; Enjoyed every; You always.

Al: Regarding people. O for one; T for that’s all I have; H, hope you continue- and so on. Very clever.

Andi: He did actually manage to get Roth IRA in there.

Al: He sure did.

Joe: I have no idea what the question was. So if you’re going to die at 80, you start at 50, how much money can you spend? Is that the question?

Al: Yeah that’s the question. Is there like a percentage?

Joe: Yeah. I don’t know. 50? 3%.

Al: Well, I’ll tell you when you’re 79, you can spend 100% of what you have. And then you just work backwards from there. It depends. It depends. Right? It depends how much you have and what your rate of return is and what the sequence of returns is. It’s an impossible question to answer. But I like it.

Joe: So bad.

Al: I mainly like the haiku. Hey, Roth IRA.

Joe: I don’t think he even paid attention to the question that he-

Al: No, he was just trying to get that-

Joe: Exactly. You know, that’s all for now. Just a random, selfish, grim question. What the-

Al: He had to keep adding paragraphs that get the IRA part. In case you missed it. And then really smart. Always. Will. That’s- I for one-

Joe: This is the guy that siphoned the gasoline.

Al: That’s right. Exactly. You can tell the guy-

Andi: That’s what you thought that he did. That’s what you came up with, which made it so funny.

Joe: Andi, read his email. The guy drinks gasoline on Friday nights. He is getting hammered on gas.

Al: It’s why he doesn’t have to spend a lot. He’s got free alcohol.

Joe: Oh man. Yeah. Will’s got- he’s got a gas problem. He’s got- he’s got a problem.

Al: And so I’ll continue. So at 100- I mean it at 79, you can spend all of it, at 78 you spend half of what you have, save the other half for next year. At 78, spend 1/3 of it. 1/3, 1/3, 1/3.

Joe: There you go.

Al: Just worked backward.

Joe: Yep. And then you’ll finally get to a certain percentage.

Al: Yeah right. How about that?

Joe: All right. We’ve got to take a break. Thanks for the little haiku. Very clever Will, always appreciate you writing in.

See Will’s secret message within the transcript of today’s episode by clicking the link in the description of today’s episode in your podcast app. While you’re there, download Big Al’s Quick Retirement Calculator Guide to find out how ready you are for retirement. First, go to the podcast show notes at YourMoneyYourWealth.com and download Big Al’s Quick Retirement Calculator Guide- it’ll help you ballpark how much income you’ll need from your investment portfolio in retirement. Then, click the Ask Joe and Al on Air button in the podcast show notes and send in your situation to have the fellas spitball for you. Or, you can skip over all of that and click the big green “Get an Assessment” button at the top of the page to schedule a free, comprehensive and personalized one-on-one financial assessment with a CERTIFIED FINANCIAL PLANNER™ on Joe and Big Al’s team at Pure Financial Advisors. There is no cost or obligation and it’s pretty likely that they can find ways to get more out of your retirement portfolio and plan. Just click the link in the description of today’s episode in your podcast app to get the process started.

Why Track Basis, Gains, and Losses?

Joe: All right. We got Perry from Jersey, “I live in Jersey. Am I paranoid?”

Al: Probably.

Joe: I don’t know.

Al: We’ll see.

Joe: “69 yo; Dog, Schnoodle; single; vehicles-” he’s got a small fleet.

Al: Nice.

Joe: Nice, Perry. Lovin’ it. What do you think constitutes a small fleet?

Al: More than one. Probably a car and a motorcycle.

Joe: I would say it’s- I would say more than three.

Andi: That’s what I was thinking too.

Joe: Right? I would say a couple of cars is 2. If I have 4 or 5 cars, I’m seeing a fleet.

Al: I think a car, a motorcycle and a Vespa.

Joe: “I’m investing much of my savings with Ameriprise.” Since the IDS days-” I’m all too familiar with that company there Perry from Jersey, that’s where I started my career. IDS, American Express Financial Advisors, right there Minneapolis, Minnesota, home office, downtown. I worked in the New Brighton office. So say hello to Ameriprise advisor in New Brighton, Minnesota. “When I review my account online, as expected, my non-qualified brokerage account shows much data including cost basis in unrealized gain or loss. Question 1. Why does my Roth contributory IRA, my Roth conversion IRA, and traditional IRA also track record 40 years of cost basis and unrealized gain/loss? Do accountants just love numbers so much that they spend their free time recording them?

Al: We- the answer is yes on that one. We do.

Joe: “Or is the IRS requiring this data for a future tax grab like unrealized Roth long term gains. Why are they keeping track of this historical data?” What say you, Big Al?

Al: Well, cost basis- I understand that because if you’re under 59 and a half, you can take out your cost basis.

Joe: It’s FIFO tax treatment in a Roth.

Al: That’s right. But you have to know how much you can take out and you know the cost basis to do that. Once you’re over 59 and a half, the only reason cost basis is important is if you just started your Roth IRA and you haven’t met the 5-year clock. So why there’s an unrealized gain/loss in a Roth? There’s no tax reason. I think that’s just for investment tracking. I’m guessing. I don’t know.

Joe: You know what I think they did? This is a total hypothetic- this is a guess.

Al: OK. Well, so was mine.

Joe: I know. Oh boy. Is they have a system with all of their accounts. And they probably just-

Al: Whether it’s Roth or not.

Joe: Right? Maybe it’s too expensive to shut it off on other accounts so they just run it on all. Because I know custodians had to change it- the whole tracking of basis a few years ago is a big deal now with custodians. So a lot of custodians had to go back and individuals had to put their cost basis in. And so the IRS came down on these custodians to make sure that they’re tracking cost basis appropriately. So yeah, there is no tax reason from a Roth IRA.

But you’re right, it’s probably to track FIFO tax treatment, first in first out. What have you contributed? What is the growth? You could take your earnings out last.

Al: It’s also kind of cool to have it, I think. So then you know how much your account appreciated. It’s not taxable, but at least you know.

Joe: I suppose in a brokerage account. if you don’t have an advisor that’s giving you that information. If it’s a brokerage account. they probably don’t have- here’s your annual return. You got to kind of figure it out yourself. And so-

Al: Here it tells you that. I mean I kind of like that.

Joe: Well, you’re an accountant.

Al: Yeah but I like numbers and I spend my free time recording them.

Joe: “Question Two. My discharged advisor-” what the hell is a discharged advisor?

Andi: Fired.

Al: Advisor he fired.

Joe: Oh he fired. Look at Perry.

Al: Or he was- the advisor was discharged of his license because of-

Joe: – fraudulent activities?

Al: – some egregious thing.

Joe: Got it. “My discharged advisor suggested I consolidate my contributory IRA and Roth conversion IRA into a single account. Is this kosher? Is there any advantage other than a less lengthy statement? Your loyal and obedient servant. Perry.” Perry, you’re paranoid. I mean he’s firing his poor advisor because he asked him, ‘hey you know what? Maybe we should consolidate these two accounts for you. What? Fired.

Al: Yeah. You’re absolutely right.

Joe: Why do you have cost basis on my Roth IRA? Fired.

Al: Why is there unrealized gain/loss? You’re right. So I think when he says contributory IRA, he means contributory Roth IRA.

Joe: Yeah. That’s what he means. Roth contributory IRA.

Al: I think that’s what I mean.

Joe: And Roth conversion IRA.

Al: And yeah, go ahead and consolidate. Make it simpler. What’s the difference?

Joe: There’s a 5-year clock on conversions and there’s a 5-year clock on regular Roths, depending on your age. Right. So if you do a conversion, each conversion that you make into a Roth IRA has its own 5-year clock, if you’re under 59 and a half.

Al: Right. He’s 69, so it doesn’t matter. Perry, you’re 69 yo.

Al: Let it go.

Joe: Let it go bro. Relax. Maybe hire your discharged advisor back. You’ve been with him for 40 years. Yeah. I never trusted that guy. The last straw-

Al: And now he’s telling me to consolidate.

Joe: The last straw.

Al: What’s his angle?

Joe: Asking me to consolidate my Roths. How dare he? Should I call the SEC on him?

Donating Stock Upon Death

Joe: All right. “Joe, Joe’s sidekick and Joe’s assistant.” Oh, look at that.

Al: How about that? I got demoted.

Joe: I love this kid. Who’s this? Tom, from the Chicago area. Again. All right Tommy. “Still married, still 60, still driving my Civic-”

Al: – still working-

Joe: “- still working, still don’t have a retirement dog, still running, even in Chicago. It’s cold as hell. Listening to you guys several times a week. I have two questions for Joe, Al and awesome Andi.” He’s funny.

Al: Yeah. Well, plus he’s he totally stroked your ego so you love him.

Andi: Oh yeah absolutely.

Joe: Dude, I don’t care what he says.

Joe: He’s gonna ask me like 15 Roth IRA conversion questions and I’ll answer every single one of them.

Andi: Ah, folks. Now you know the secret.

Al: Just call me a sidekick and Andi an assistant.

Joe: Yep. “I’ve heard that there can be tax advantage for heirs if I plan for my estate to donate stock from my IRA directly to a charity upon my death. I can see the advantage of donating stock to a charity while I’m alive which allows the transaction to be free of capital gains for everyone. However, I don’t understand the possible advantage for my heirs when I die. Can you explain that if this is true? And any potential perils or entanglements. Does it matter if the IRA holdings are in individual stocks or mutual funds? Also does it matter if my spouse outlives me?? Let’s pause there. So my boy Tom is getting some advice. And he’s saying you know what? If you give money to a charity at your death that will save your heirs money in taxes. And the answer to that question is true.

Al: It depends.

Joe: Well, because they don’t have the assets.

Al: So they won’t pay any taxes.

Joe: So they won’t pay any taxes-

Al: They won’t ever pay any taxes on it.

Joe: – so you don’t wanna give your assets away to avoid taxes. Do you want to pay maybe 20% of tax or give 100% of it away, Tom. So yes, it will save you taxes.

Al: Well so- let me sort of expand on that because there’s two kinds of taxes you could be talking about. One is the estate tax but that would mean your estate would have to be over $11,500,000.

Joe: If you’re married, $22,000,000.

Al: That’s correct. So gigantic estate. If you’re going to give some assets away, you give your IRA assets. But more than likely most people don’t have $11,500,000 per person. Most people- maybe Tom does- but most people don’t. And so the reason why you would give your IRA assets to charity is if you want to give money to charity anyway upon your death, you’d rather give them the IRA and give your beneficiaries the non-IRA. Because that will be less taxing for them. But that’s only if you want to give to charity.

Joe: Right. If you don’t want to give to charity-

Al: – then forget it.

Joe: So the IRA has income tax consequences at your death. There’s no stretch IRA any longer. So when you pass away the heirs, the beneficiaries will have to deplete the account within 10 years. So if Tom’s got a ton of money in there, then the kids will have to deplete it. It’s all ordinary income so no matter- I’m sure Tom’s kids are pretty talented, just like Tom is. So yeah, they could probably lose a little bit of money in tax. The other assets would get a full step-up in tax bases, so they could sell those assets right after Tom passes and not pay a dime in tax.

Al: Yes. So just- I’ll try to say it simply- if you have a certain amount of assets and you want some to go to charity and some to go to your kids, then you would favor the charity getting the IRA assets. Because then that’s taxable. Charity doesn’t pay tax on it cause they’re a non-profit. But your kids would if they receive it. So you’d rather give your kids than non-IRA assets, if you have a choice, if you want to give to charity.

Joe: “Does it matter if my spouse outlives me?” Well sure. You would want to name your spouse the beneficiary. If you named the charity the beneficiary, she will have to sign off on that. She doesn’t have any of the assets. It just goes to the charity. So be careful there.

Does My Financial Advisor’s Location Matter?

“Another unrelated question- one other unrelated question- I’ve also heard that it is advantageous to pick a financial advisor that is based in the state I plan to retire in. Wondering if you have thoughts on that? Perhaps I can ask Roth conversion question next time.”

Al: You opened it up for him. You told him he could.

Joe: Anytime, Tom. Anytime, Tommy.

Al: What do you think? Do you pick an advisor on the state you retire in?

Joe: I don’t know. Why does it matter?

Al: Yeah. I don’t care either. The only reason you pick an advisor in your own state is just if you want to see him or her, it would be more convenient.

Joe: – in person.

Al: Yeah, right. Nowadays with Zoom, it doesn’t really matter.

Joe: The only other advantage I can see is that if I’m an advisor in Illinois versus California, I probably know Illinois tax law a little bit more.

Al: And I might understand Illinois estate taxes better too.

Joe: So if I had a client that lived in Illinois that I was servicing, I would be pretty tight on Illinois tax.

Al: Probably would learn about it.

Joe: I would ask Big Al.

Al: And I would call some CPA that has nothing to do but record numbers in his spare time.

Joe: So here’s my advice Tom, if you want to find a good advisor, I would a) seek out a CERTIFIED FINANCIAL PLANNER™. Seek out someone that is fee-only. Seek out someone that has expertise in what you’re trying to accomplish. I think the advisor that you’re seeking advice from with this whole give your IRA to charity to save money in taxes, maybe bypass that individual. No offense. But yeah.

Al: I think- I also think it’s easier to find that advisor in your hometown, get to know that person. And then when you move out of state you’ll already have that relationship. It’s a little bit harder. It’s not impossible. We personally have clients across the country. So it’s not impossible.

Joe: Are you selling Tom to become a client?

Al: Not really. Because he’s only going to listen to you. Because I’m apparently just a sidekick. But the point is you can meet advisors over Zoom and we’re doing a lot of that ourselves, as are other advisors. But there’s something to be said for getting to know a person, having a relationship before you move to another state. That’s just one thought.

Joe: Yeah. But the relationship is key of course, but you want to make sure that they’re competent.

Al: Of course.

Joe: I mean we see a lot of cases that come through our desk and it’s like wow this is really bad advice and it’s like ‘I’ve been with Johnny for 30 years.’ It’s like ‘well Johnny’s not that great of an advisor.’ We got a very small dent in the emails today but we’re working on it. Keep ’em coming, go to YourMoneyYourWealth.com if you have a money question and we’ll see you all again next week

_______

Derails comin’ right up!

Subscribe to the YMYW podcast newsletter

FOLLOW US: YouTube | Facebook | Twitter | LinkedIn

Your Money, Your Wealth® is presented by Pure Financial Advisors. Sign up for your free financial assessment.

Pure Financial Advisors is a registered investment advisor. This show does not intend to provide personalized investment advice through this broadcast and does not represent that the securities or services discussed are suitable for any investor. Investors are advised not to rely on any information contained in the broadcast in the process of making a full and informed investment decision.

Listen to the YMYW podcast:

Amazon Music

AntennaPod

Anytime Player

Apple Podcasts

Audible

Castbox

Castro

Curiocaster

Fountain

Goodpods

iHeartRadio

iVoox

Luminary

Overcast

Player FM

Pocket Casts

Podbean

Podcast Addict

Podcast Index

Podcast Guru

Podcast Republic

Podchaser

Podfriend

PodHero

podStation

Podverse

Podvine

Radio Public

Rephonic

Sonnet

Spotify

Subscribe on Android

Subscribe by Email

RSS feed

YouTube Music