With the consumer price index at forty-year highs, this is a good time to take a look at what types of investments might make sense in an inflationary environment. Before diving in, though, it’s important to note that there are no foolproof methods to avoid short-term surprises. The bottom line is that if inflation readings come in higher than expected, most major asset classes are likely to suffer. However, as your time horizon stretches out, you can take steps to position your portfolio for optimal performance in an era of rising prices, so that is what we’ll focus on. Watch the video:

Stocks

As mentioned above, if a monthly consumer price report comes out much higher than expected, the broader stock market averages aren’t likely to do very well that day. But in the long run, the stock market represents a collection of companies, and many good companies have loyal customers and a degree of pricing power. For instance, if you love watching Stranger Things, you’re unlikely to cancel your Netflix subscription if the monthly cost increases slightly. Similarly, fans of Disneyland will still visit the park even if the entrance fee goes up.

As an investor, that means that good companies should continue to generate profits, even in an inflationary environment. And corporate profits, more than anything else, are what drive stock price returns.

Of course, some companies will struggle. Their cost of goods sold might increase at an unsustainable rate. Or they might find themselves unable to pass cost increases along to customers. That is the nature of capitalism; some companies fail while others succeed. That is why we suggest owning a broad swath of companies, whether through a diversified collection of individual securities, or a low-cost mutual fund, or an exchange-traded fund (ETF.) The bottom line is that a portfolio of high-quality stocks is likely to provide your best odds of keeping pace with, or even exceeding, inflation over the long run.

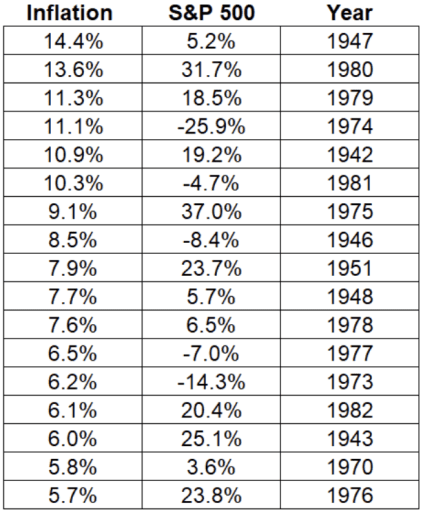

Here is a chart showing the years with the highest inflation and the corresponding stock market return that year. As you can see, there were some down years and some up years. The average return in those years was 9.4%, which is pretty close to the average stock market return across all years. Those numbers provide compelling evidence that stocks can effectively hedge inflation over time.

Natural Resources

One subset of stocks that bears a closer look is natural resource producers. Companies in industries such as oil, gas, agriculture, metals, and farming have historically done well during periods of inflation. This is partly because the commodities the companies sell tend to increase in price alongside inflation, leading to increased revenue to offset any increased costs. It could make sense to hold natural resources companies in your portfolio, particularly if inflation remains high.

A couple of caveats are in order, though. When we discuss natural resources, we specifically refer to companies involved in these industries. We aren’t proponents of the actual raw materials themselves due to their volatility and the difficulty in getting accurate exposure to their underlying price movements. Furthermore, even when investing in natural resource stocks, it’s important to size your position appropriately. These companies represent a small subset of global corporations and should only constitute a small portion of a diversified portfolio. Concentrating on any sector, including natural resources, seldom ends well.

Bonds (Fixed Income)

The greatest risk to fixed-income investors is inflation in the absence of a default. That is because, as the name implies, the return on most bonds is “fixed.” That means that higher inflation leads to less real purchasing power over time. Because of this, bonds are sensitive to changes in actual or expected inflation rates.

However, just because we are in an environment of high inflation doesn’t mean that you shouldn’t own any bonds. For starters, bonds are generally less volatile than stocks, so many investors should hold a percentage of their overall allocation in bonds for diversification and relative stability.

The key is to hold the right types of bonds. When inflation strikes, the greatest losses are in bonds with the longest maturities. This makes sense since inflation has more potential to erode purchasing power over longer time frames. So, in inflationary environments (and in most non-inflationary environments, too), investors should focus their bond portfolios on securities with short or intermediate-term maturities. Doing so generally allows investors to capture the majority of bond market returns, while also moderating inflation and interest rate risk.

I Bonds

A surge in inflation has seen a corresponding increase in inquiries about I Bonds. As a reminder, I Bonds are issued by the U.S. Treasury, have 30-year maturities, and pay interest based on a combination of fixed and inflation rates.

Some of the benefits of I Bonds include:

- They are government guaranteed

- Interest is exempt from state and local taxes (but taxed at the federal level as ordinary income)

- Interest is also federally tax-exempt if used for higher education expenses (MAGI limits of $98K single/$155K MFJ)

- The current rate is more than 9.0% per year

Some of the drawbacks of I Bonds include:

- They are completely illiquid for the first 12 months, and if redeemed within five years, you sacrifice three months’ interest

- While the current yield is attractive, the actual fixed rate is zero, and historically the combined rate hasn’t been that great

- In 2015, the actual combined interest rate was zero, and the return could be zero again if we get price stability or deflation

- Purchases are limited to $10,000/year with a potential for an additional $5,000 by using your tax refund

The bottom line on I Bonds is that the current rate is attractive and should remain so for the next 12 months or more. Just keep in mind that the rate isn’t guaranteed forever and that the bonds are illiquid for a period of time. Also, because the amount you can purchase is limited, you’ll likely still need to consider other investment vehicles for the bulk of your portfolio.

Gold and Crypto

Some investors have traditionally viewed gold as an inflation hedge, and more recently, cryptocurrencies have joined this conversation. The idea is that inflation erodes the value of the dollar, which means that other “alternative” currencies should do relatively well.

The problem with this theory is that recent events haven’t supported it. The last twelve months have featured the highest inflation readings in forty years, but here are charts of the performance of gold and bitcoin.

Gold

Crypto

As you can see, gold is down slightly in the last twelve months. And since March 2022, as inflation has skyrocketed, gold has fallen more than 20%. Bitcoin has performed even worse and is down significantly for the year. That doesn’t mean gold or Bitcoin can’t play a role in a diversified portfolio, provided the position is sized appropriately. But it does mean that counting on these assets to provide shelter in a storm of inflation may not always work out as intended.

In fact, when inflation is raging, there may not be any place to hide out, at least in the short term. But the good news is that most financial goals call for a long-term time horizon, and as we’ve discussed, there are ways portfolios can be positioned for success, even in times of inflation. The key, as is so often the case, is to ignore the market volatility inflation can prompt. Instead, stick to a well-diversified portfolio that includes asset classes that have historically succeeded regardless of the inflation environment. Such a portfolio could be volatile in the short run, but it should position you for success across time, even if consumer prices remain elevated.